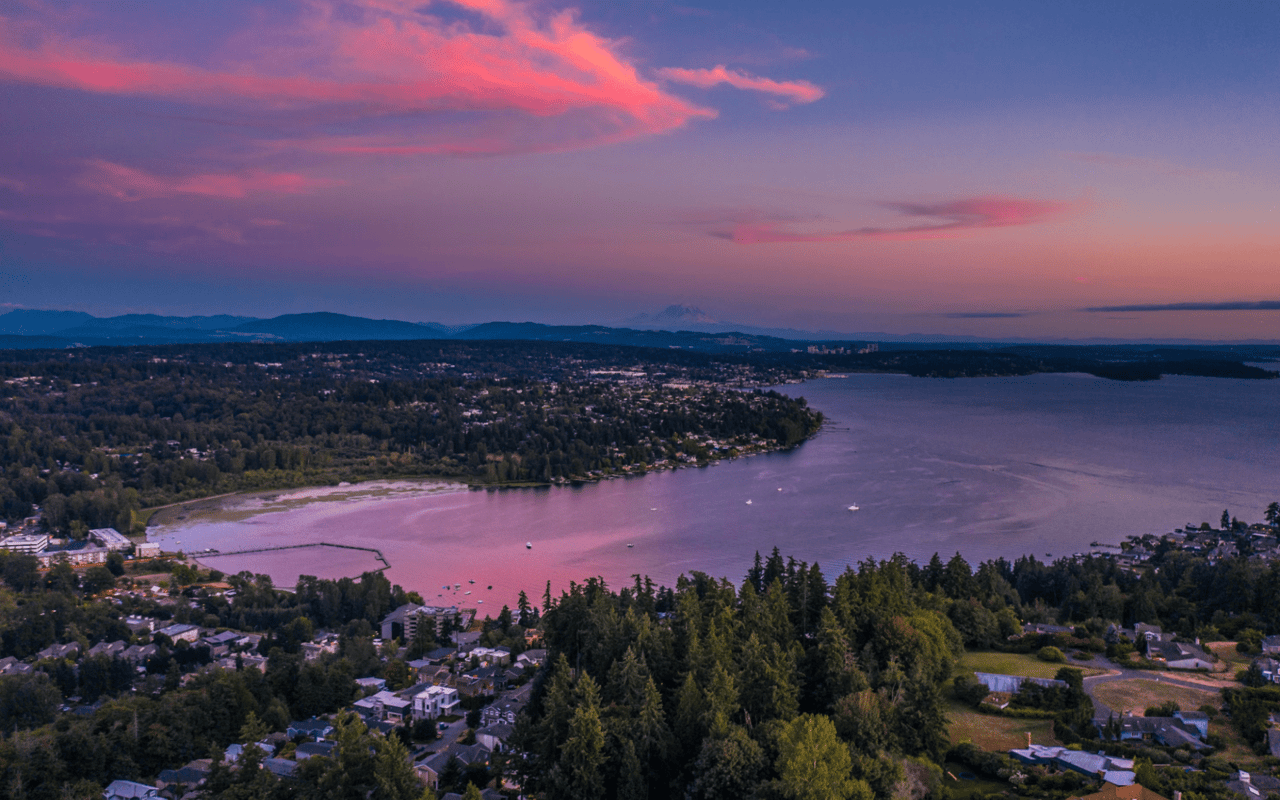

Just across Lake Washington from Seattle is an area that locals commonly refer to as the “Eastside.” These rapidly growing suburbs feature various neighborhoods, outdoor recreation, exceptional dining, major employers, and more. Eastside has grown tremendously over the last several decades, with new employers taking root and growing the economy and job opportunities. What once were small logging and mining towns quickly expanded when the amenities, housing, and services took over and transformed the area. As a result, the area has a continually expanding dining scene, community events, recreational activities, and high-end shopping.

The Eastside is an affluent area with some of the best educational opportunities, well-kept neighborhoods, impressive city centers, and stunning scenery. Many things make buying a home in Eastside wonderful. To get started, let’s discuss what makes buying a home in Eastside a great choice; then, we’ll provide tips on how to make it a seamless process.

Why should you buy a house in Eastside?

Stunning scenery

The unique landscape surrounding the Eastside is one of the biggest draws for those looking to purchase real estate. Each city offers access to explore mountains, lakes, parks, and trails. While there has been significant development in the area through the years, there is a priority placed on preserving the natural beauty of the area.

Four seasons

One of the most appealing parts of living in Eastside is that you can experience all four seasons. The summer heat isn’t overwhelming, and winter nights don’t often drop below freezing. While there may be significant rain, it’s not as dreary as people think, and the weather is often an important reason people flock to the area.

Excellent education

Whether you have children or you want to focus on higher education, the educational opportunities in Eastside are endless. This area features some of the top-rated school districts in the state and the nation. Not only are they consistently top-rated, but they are award-winning institutions that range from public to charter and private schools. You’ll also find an assortment of higher education, including Bellevue College, Northwest University, and Seattle University.

Top neighborhoods in Eastside

Woodinville

This neighborhood is in the heart of the Sammamish River Valley and is known for being a successful part of Washington’s wine country. You’ll find an abundance of scenic farmland, bike trails, and trendy breweries here.

Kirkland

Sitting on the eastern shore of Lake Washington is the gorgeous town of Kirkland. Often claimed as the Eastside’s first “waterfront destination,” you’ll find its lakeside downtown the perfect spot to explore galleries, local boutiques, fine dining, and more.

Bellevue

Bellevue is the largest of the cities on the Eastside and offers the most stunning view of the downtown skyline. You’ll find easy access to Lake Washington, high-end shopping and dining, and the third-largest higher education institute in the state.

Redmond

Redmond is a budding technology town best known worldwide as the home of Microsoft. The evolving downtown core offers outdoor recreation, shopping, and dining options. The local Marymoor Park is a significant attraction in the area and hosts several events like summer concerts, sports tournaments, and cycling events.

Types of home loans for all homebuyers

Conventional loans

The most common type of fixed-rate mortgage, and the most accessible, is the conventional home loan. Buyers can choose between a 15-year or 30-year fixed-rate mortgage, which guarantees the interest rate remains the same through the life of the loan. A 30-year loan is beneficial because your monthly payments will be lower, but a 15-year loan means you’ll pay less interest throughout the life of the loan.

FHA loans

FHA loans are a popular choice among first-time buyers because they require only a 3.5% down payment, which is significantly less than the commonly recommended 20% down payment. While there are many perks, there is a downside to this loan, though. Because of the added risk to lenders, FHA loans require you to hold private mortgage insurance (PMI), increasing your monthly payments.

VA loans

VA loans are specifically for service members and their families. While they are similar to conventional mortgages and can be backed by various lenders, you must meet minimum service requirements to obtain one. One great part of VA loans is that you aren’t required to make a down payment or hold additional insurance. However, there are several drawbacks to this type of loan. First, although you won’t have to make a down payment, you’ll need to pay a VA funding fee which covers the cost of a potential foreclosure. Additionally, you’ll need to have a VA-endorsed appraiser evaluate the property and deem it worthy of the loan.

Money-saving tips for buying a home

Get pre-qualified or pre-approved

One effective way to determine what size mortgage you can financially handle is by getting pre-qualified. During a pre-qualification, a lender performs a soft credit check and thoroughly examines your proof of income. This helps them determine whether you can financially handle the cost of the mortgage. While that’s an excellent place to begin, getting a pre-approval will go deeper and give you a more accurate picture. A pre-approval shows sellers that a lender has given them the green light and they are serious about purchasing a home.

Consider a more significant down payment to keep monthly costs down

The cost of a down payment varies based on the price of your home and the type of mortgage you have chosen but is typically between 3% and 20% of the home’s purchase price. Whether you have to pay a down payment or not, paying at least some will benefit you greatly. The larger the down payment, the smaller the loan, saving you money. If waiting is an option and you can save more money, that might be beneficial to you.

Increase your credit score

Another thing that buyers often overlook is their credit score. A higher credit score will help keep your rates and payment lower. Buyers with 700 or higher credit scores are often seen as worthy by lenders and will get better rates. If your score isn’t in good standing, there are several ways to ensure you get it to a good place. To begin, pay off your credit cards, or keep them minimally used. A general rule of thumb is keeping the utilization rate beneath 20%. It doesn’t take long to bring your credit score up and within an acceptable range, so take a few months to work on it, if necessary.

Are you ready to find your dream home?

If you’re ready to call Eastside home, it’s time to start looking at Eastside real estate. Contact Kevin Donovan today to begin the search. With over two decades in the industry and countless real estate transactions closed, you can be sure you’re in trusted hands.